If you have your own small business or if you’ve ever dreamed about starting one, you know what an exciting and daunting experience it is. One of the most important and often most overwhelming aspects of starting a business, is making some decisions about the financial side of things. If you don’t have a bookkeeper or accountant on hand, this might feel quite out of your depth. However, there are several steps that even the most inexperienced business owners can take to ensure their company doesn’t get into any unwanted trouble with the authorities.

Think about getting a bookkeeper

Do some research into the benefits of hiring a bookkeeper. A bookkeeper can help you keep track of your finances and make sure everything is in order, so it is often worth the cost if that isn’t something that comes naturally to you. Bookkeepers take care of recording the everyday financial transactions of a business. If you don’t have access or the resources to hire a bookkeeper just yet, there are software programmes that can guide you in setting up your accounts and keeping track of everything. We’ll go into more details later on in this blog post.

Look into getting an accountant

An accountant can generate reports you need to submit for legal requirements for your business and they are also able to analyse and give insight into these reports. Accountants perform audits and file tax returns on your behalf. Whereas a bookkeeper is more administrative and works with recording daily financial transactions, an accountant might play a more strategic role for your company. An accountant will also make sure that all the financial reports provided are accurate and complete – something that can be difficult for small business owners who may not have detailed knowledge about accounting procedures or the laws surrounding them.

While it is clearly beneficial to work with a bookkeeper and an accountant, or at least one of them – that is not always possible at the outset of starting a business. Make sure you know all the legal requirements you need to adhere to and put everything in place to stick to them. As mentioned previously, we’ll share some software programmes later in this blog post that can help in setting up accounting tools for your small business.

Laine Redpath

Laine Redpath

How do I get started with accounting for my small business?

If you have the time and energy (after running everything else business-related) and you also understand the basics of accounting you can probably go ahead and start your small business’s accounting yourself! Alternatively, as we mentioned above, you can think about hiring a bookkeeper or accountant or even looking into various accounting software programmes.

Know your expenses

The first step in the financial health of your business is knowing your expenses. Expenses can be broken down into two types: fixed and variable. Fixed expenses are those that do not change based on sales volume, such as rent or insurance premiums; variable expenses are those that increase or decrease depending on how much product you sell, such as payroll costs for employees who work at different times throughout the year. When you have a clear understanding of these categories of costs, you will be able to understand when to hire more employees or buy more equipment if necessary when sales increase. And you’ll also know when to rather wait to make changes in order to keep your business comfortably afloat.

Register your business

You will need to decide on the format and type of registration for your small business. In the UK the most common way of doing business is to register as a limited liability company, or LLC. An LLC is more flexible than a corporation and allows owners (the "members") more control over their own profits and losses. However, there are also downsides: if you dissolve an LLC or sell it, you will have to pay taxes on any gains made during your ownership period as well as any remaining cash on hand at that time.

You can find more information and register your company via the gov.uk website.

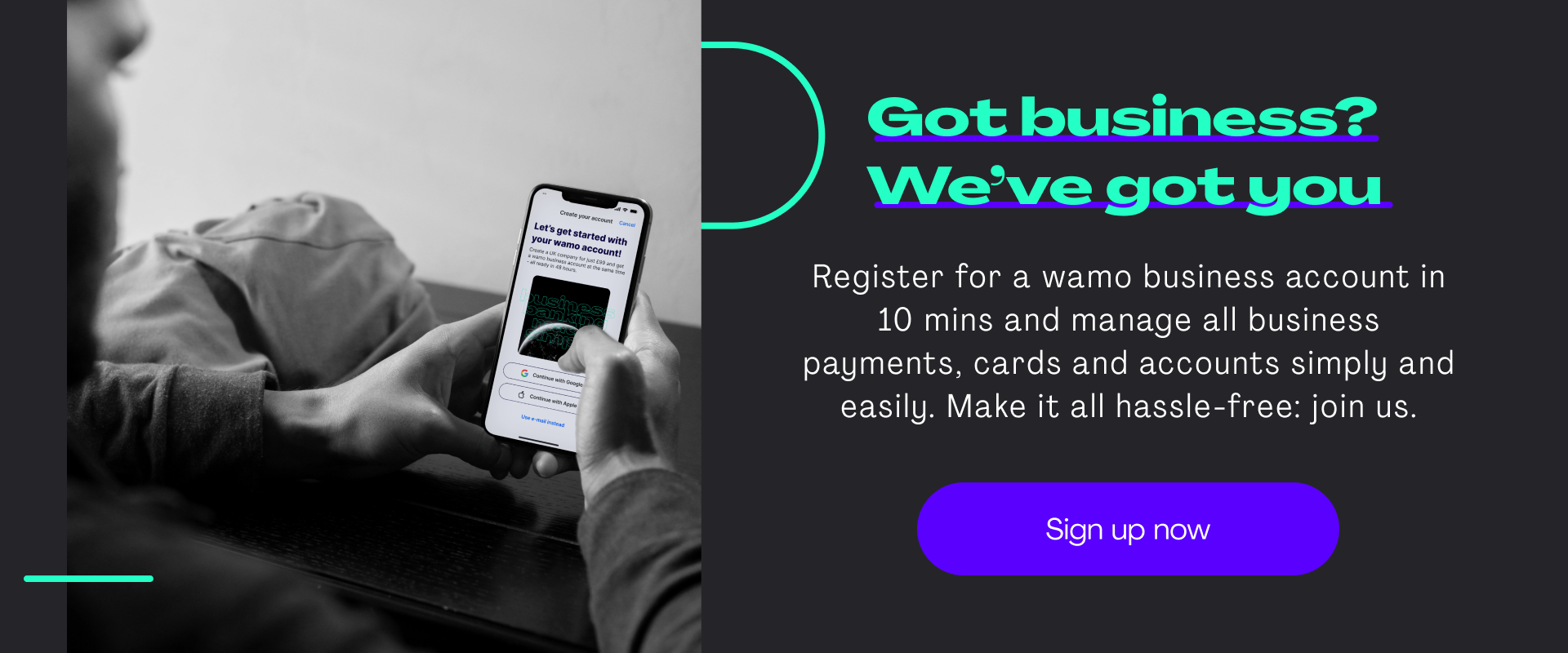

Set up a business account

One of the first things you’ll need to do when running a business is set up a business account to pay for your business expenses. You will need to keep track of all your business transactions carefully. Having your accounting system in place will prove vital to know your expenses from transactions and other income.

You'll also need to reconcile your bank statements regularly. Reconciliation refers to comparing the balance on an account statement with what is actually in that account at that time – in other words, making sure there are no errors between what appears on paper versus reality. Inaccuracies can occur when someone makes changes directly through their online service or via phone call with customer service representatives, who may not always understand exactly what they're doing!

Your business account will be used to track your income and expense accounts. You'll be able to pay your expenses out of the income account, and you'll be able to deposit your income into the expense account. This is a good idea because it helps keep track of how much money you have left over at the end of each month by reconciling both sides of your balance sheet (assets vs liabilities).

There are many options of where to set up a business account. You could go for the more traditional high street banks, although these often have higher fees and longer waiting periods. There are many newer platforms with products and features specifically designed for small businesses and entrepreneurs. You can open a business account through a financial service provider like wamo in just 10 minutes. Take a look at wamo’s subscription plans here.

If you want to run a small business successfully, it's important to keep good financial records!

In order for your business to grow and flourish, you need to have a clear understanding of where all the money is going. This means that you need to keep track of how much money comes into the company and how much goes out – and that's where accounting comes in. Accounting refers to the process of recording financial transactions and preparing reports based on those transactions. As we saw earlier on, there are two key methods to keep track of your finances: bookkeeping (which involves simpler, day-to-day record-keeping) and accounting (which involves more complex analysis and reporting).

Sinan Elver

Basic accounting terms to familiarise yourself with

Accounting is a language of its own. And just like any other language, there are certain words and phrases that are used to communicate with each other. We won’t go too in depth describing all the accounting terms that are helpful for a small business owner, but here are some words and terms you can look up online to familiarise yourself with the basic concepts: Asset, Capital, Liability, Accounts Payable, Revenue, Accounts receivable, Expenses, Gross profit, Net profit, Gross margin, Net margin, Cash flow, Inventory, Valuation, Depreciation, Break-even point, Liquidity, Overhead, Accounting period, Cash flow statement, Balance sheet and Income statement.

How often should I keep track of my small business’s accounting records?

It depends on the nature and size of your business. If you are a one-person operation, it's possible to keep daily records and update them regularly. However, if you have multiple employees or complex accounting needs (such as inventory tracking), weekly or monthly updates may be more appropriate. The important thing is that whatever time period works best for your company is also the most efficient way to maintain accurate records that can be used in tax preparation at year end.

Software accounting designed to help small business owners thrive

When you're just starting out, it's easy to get overwhelmed by all the numbers. But don't worry – there are plenty of tools out there to help you manage your finances.

One important thing to keep track of is reconciling your accounts each month. This means comparing what's in your account with what your accounts say. There are many useful software programmes that can help you with this. If there are differences between what's on paper and what's actually sitting in your account, make sure you know why they exist before moving forward!

Accounting software available for small businesses

Small businesses are some of the most important companies on the planet, but they're also some of the most under-served and under-supported. That's why it's so important for small business owners to find the best accounting software for their needs. Good accounting software will help you keep track of your finances and make sure that you're staying compliant with all applicable regulations and laws. Below are just 5 examples of accounting software out there available to help you run your small business.

1. Xero

Xero is a cloud accounting software for small businesses. The app was founded in 2007 by New Zealand natives, Rod Drury and Kaye Adams. The company has since grown to become one of the most popular online accounting services in the world with over 1.1 million users worldwide, including large corporations such as Uber and Airbnb.

2. Wave

Wave is a cloud-based accounting software that offers an easy-to-use interface and has no credit card required. It's perfect for small businesses or freelancers, who need to keep track of their finances on the go.Wave has everything you need in one place: invoicing, expense tracking, bill payment and more. The best part? It's free!

3. Freshbooks

Freshbooks is an accounting software that helps you manage your time and billing. It has a simple interface and is easy to use, which makes it ideal for small businesses. Freshbooks also offers a free trial period, so you can try it out first before committing to the paid version of their services. The interface is user-friendly as well, making it easy for anyone in your company who has never used accounting software before to learn quickly how to use Freshbooks' features effectively.

4. Quickbooks

Quickbooks is a powerful accounting software that's easy to use, with a lot of features and integrations. It also has a lot of support options. Quickbooks is one of the most popular accounting softwares for small business because it has so many integrations with other apps, like ERP systems or CRM systems.

5. Outright

Outright is an accounting software for small business. It has a good user interface, and it's easy to use. You can get started quickly with Outright because it's cloud-based, which means you can access your data from anywhere. The biggest benefit of using Outright is that it gives you the power of being able to see all of your financial information in one place, and then acting on that information accordingly.

We hope this blog post has been helpful in better understanding the accounting needs of your small business. It can be difficult and overwhelming to make sure you have everything set up correctly, but these tips and tools should lead you in the right direction.