At wamo, we’re here to help your business thrive. In this series we’ll share everything you need to know about running a business out of Estonia. Estonia has become known for its business-friendly tax system, particularly when it comes to corporate tax. If you’re looking to establish your business in this Baltic nation, whether local or international, we have all the tax information you need.

The Estonian approach to corporate taxation

Estonia, unlike many countries, has a unique approach to corporate taxation. It is known as the “territorial principle”. This means that only income generated within Estonia's borders is subject to taxation. Any income your company earns through international operations and investments will remain largely untouched by Estonian corporate taxes. Here are some key things to note about the Estonian corporate tax system:

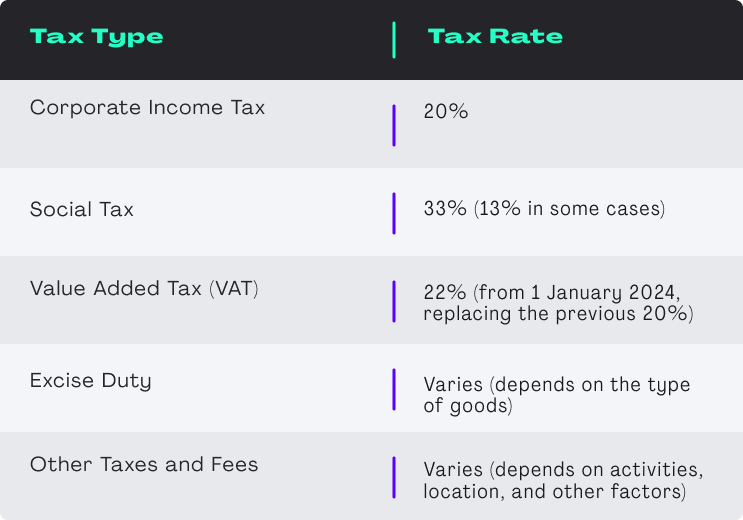

- Corporate income tax: Estonia imposes a flat corporate income tax rate on distributed profits. This rate has stayed low for quite some time, making Estonia an attractive place for businesses looking to optimise their taxes.

- No tax on undistributed profits: Unlike many countries where businesses face taxation on profits, Estonia only taxes profits when they are distributed as dividends.

- Tax credits for foreign taxes paid: Estonia has agreements with a lot of countries to avoid double taxation. Businesses can often receive tax credits for foreign taxes paid on income earned abroad.

- Transparent and efficient tax administration: Estonia's tax authority, the Estonian Tax and Customs Board, is known for its efficient and digitised services. This means it is relatively easy for businesses to comply with tax regulations.

The importance of proper record-keeping

The Estonian tax authorities place a high emphasis on transparency and compliance and it’s therefore important to be meticulous in keeping track of your tax records. Proper record-keeping means that your business will easily be able to show its financial activities and tax liabilities when they’re requested by various authorities.

Key filing and reporting dates

There are specific deadlines for the different tax-related filings and reportings. To avoid penalties and to keep in good standing with tax authorities it’s important to remember them. Here are some of the crucial dates to add to your calendar:

- Monthly tax declarations: Due by the 10th day of the following month.

- Quarterly tax declarations: Due by the 10th day of the month following the end of the quarter.

- Annual reports: Typically due by June 30th of the following year.

Resources for further information

The Estonian Tax and Customs Board provides a range of online resources, guides, and customer support services to help businesses understand and navigate the corporate tax system in Estonia. You can use these resources, or seek further professional advice, to make sure your company is tax compliant.

Exploring types of corporate taxes in Estonia

The corporate tax system in Estonia is made up of several different taxes. Each has its own unique characteristics and implications for businesses. Next, we’ll take an in-depth look at these tax types, including corporate income tax, social tax, VAT (value added tax) and other taxes and fees.

Corporate income tax

Corporate income tax is a central component of Estonia's tax system. It is worked out on the distributed profits of a company. This means that only the portion of profits paid out as dividends to shareholders is subject to this tax. Undistributed profits are not taxed. This provides a big advantage for businesses looking to reinvest their earnings.

Key points regarding corporate income tax

Flat tax rate:

Estonia applies a flat tax rate to distributed profits. This means that no matter what the amount of profit a company distributes as dividends to its shareholders, the same tax rate is applied. In Estonia, this rate has always been quite low, making it simpler for businesses to calculate their tax liability.

For example, if the flat corporate income tax rate is 20%, a company distributing €100,000 in profits as dividends would owe €20,000 in corporate income tax.

Residency of the shareholder:

The tax treatment of dividends depends on whether the shareholder is a resident or non-resident of Estonia.

Resident shareholders: If the shareholder receiving dividends is a resident of Estonia, they are typically subject to a reduced rate or may even be exempt from paying personal income tax on the received dividends. This incentivizes Estonian residents to invest in domestic companies.

Non-resident shareholders: Non-resident shareholders may be subject to a withholding tax on the dividends they receive. The exact rate and any potential reduction due to international tax treaties will depend on the specific treaty provisions and the tax laws of the shareholder's home country. Estonia often has tax treaties in place to prevent double taxation.

International tax treaties:

Estonia has entered into double taxation treaties with numerous countries to avoid a situation where the same income is taxed twice—once in Estonia and again in the shareholder's home country. These treaties generally specify how dividends, interest, royalties, and other types of income are to be taxed and provide mechanisms for providing tax relief or credits to prevent double taxation.

For example, if an Estonian company pays dividends to a shareholder in another country with which Estonia has a tax treaty, the treaty may limit the withholding tax rate on those dividends. This ensures that the shareholder isn't excessively taxed on the same income in both Estonia and their home country.

These elements of Estonia's corporate income tax system are designed to encourage investment, simplify tax calculations, and provide mechanisms to mitigate double taxation for shareholders with cross-border investments.

Social tax

Social tax in Estonia is a mandatory tax that funds the country's social security system. It is levied on the gross salaries and other benefits paid to employees. It is the responsibility of employers to calculate, withhold, and remit this tax on behalf of their employees.

Social tax in Estonia Is super important and funds pension insurance and state health insurance. The tax rate is set at 33%, although there are cases where a reduced rate of 13% may apply.

Key points regarding social tax:

Taxable Amount: Social tax is levied on income from employment and business activities.

Minimum social tax liability: Those who pay social tax are subject to a minimum rate of social tax liability. In 2023, the monthly rate on which the minimum social tax liability is based is 654 euros. This means that the minimum social tax liability for employers is 215.82 euros per month.

Calculation procedure: The procedure for calculating the minimum liability of social tax has been established by the Minister of Finance Regulation No 17 of 15 March 2013 (in Estonian).

Sole proprietors: Sole proprietors are also responsible for paying social tax. They make advance payments four times a year, by the fifteenth day of the last month of each quarter. The Estonian Tax and Customs Board calculates the final social tax liability annually based on the business income declared in the income tax return of the sole proprietor and sends a tax notice regarding any additional amount of social tax due. The deadline for the payment of additional social tax is 1 October.

Social tax is paid by various entities, including:

Employers are responsible for paying social tax on behalf of their employees. They declare and pay this tax on a monthly basis using the tax return form TSD.

Sole proprietors are required to make advance social tax payments quarterly and reconcile the final tax liability annually based on their business income.

In special cases, the state, rural municipality, or city may also pay social tax. They declare and pay this tax on a monthly basis using the tax return form ESD.

Contributions: Social tax covers various benefits, including pensions, health insurance, and unemployment insurance.

Monthly reporting: Employers are required to submit monthly reports and payments of social tax to the tax authorities.

Value Added Tax (VAT)

Value Added Tax (VAT) is a tax imposed by the state and is paid by those registered as VAT liable either when the liability arises or voluntarily. The obligation to pay VAT also arises when a person has mistakenly added VAT on issued invoices.

Key points regarding Value Added Tax:

Changes in the Estonian Value Added Tax Act: Starting from 1 January 2024, Estonia has implemented changes in the Value Added Tax Act, increasing the standard VAT rate from 20% to 22%. These changes are important for businesses to be aware of, as they impact the pricing and taxation of goods and services.

The VAT Act contains two transitional provisions related to the rate change:

Until 31 December 2025, for goods or services subject to the standard VAT rate, businesses using cash accounting for VAT may continue to pay VAT at the rate of 20% on transactions generated after 31 December 2023 if an invoice was issued to the purchaser, and the goods were dispatched or made available or the service was supplied before 1 January 2024.

The second transitional provision pertains to long-term contracts, especially those related to immovables. Until 31 December 2025, taxable persons can apply the 20% VAT rate, based on a written contract concluded before 1 May 2023, provided that the contract specifies the inclusion of VAT at a rate of 20% or adds VAT at the rate of 20% to the price. The contract should not provide for a change in the price due to a potential change in the VAT rate.

Changes in VAT return and data transmission:

In connection with the amendments to the Value Added Tax Act taking effect on 1 January 2024, there will be changes in the VAT return form and in the structure and specifications of the data transmission file. These changes should be taken into account by businesses when fulfilling their VAT reporting requirements.

Other corporate taxes and fees

As well as the main corporate taxes we’ve mentioned, businesses in Estonia might also come across other corporate-related taxes and fees that could include:

Local corporate taxes: Some municipalities in Estonia impose local corporate taxes. These are separate from national corporate income tax. The rates and rules for local corporate taxes may vary from one municipality to another.

Dividend tax: While Estonia's corporate income tax system is known for its unique approach, the taxation of dividends to shareholders may have implications. Understanding how dividends are taxed at both the corporate and individual levels is important for your business.

Transfer pricing documentation: Businesses involved in transactions with related entities, especially those in different countries, may need to adhere to transfer pricing regulations. This involves ensuring that transactions between related entities are conducted at arm's length, and appropriate documentation is maintained to demonstrate compliance.

Employment-related taxes: Employers have obligations related to payroll taxes. This includes income tax withheld from employees' salaries and contributions to various social security programs.

Customs duties and import taxes: Businesses engaged in international trade may encounter customs duties and import taxes. These can impact the cost of importing goods or materials.

Real estate tax: Companies that own or use real estate for their operations may be subject to real estate tax (property tax).

Stamp duty on corporate transactions: Certain corporate transactions, such as mergers and acquisitions, may be subject to stamp duty or other transaction-related taxes.

Environmental fees: Companies involved in activities with environmental impacts may be required to pay environmental fees. This is especially the case if they generate waste, emissions, or engage in activities affecting the environment.

Tourism-related taxes: Businesses in the hospitality and tourism sector may need to collect and remit tourism taxes, especially if they provide accommodations or related services.

Financial transaction taxes: Depending on the nature of their financial activities, businesses may encounter financial transaction taxes on securities transactions or other financial instruments.

Here is a summary table of the corporate tax rates in Estonia:

Strategies for optimising corporate tax liability in Estonia

As we’ve pointed out, Estonia is a great place to run a business from as it offers unique opportunities to optimise your business’s tax liabilities. We’ll explore some key strategies to help you out with this:

Profit distribution vs. retention

Estonia's tax system only imposes corporate income tax when profits are distributed as dividends to shareholders. Retained earnings are not subject to taxation until they are distributed. Therefore, businesses can employ strategies to determine when and how much to distribute as dividends, allowing for tax deferral and capital reinvestment.

Strategy: Evaluate the company's financial needs and future growth prospects. Consider keeping profits for reinvestment in the business when capital is required for expansion, research and development, or other strategic initiatives. Distribute dividends when shareholders require income, and when tax planning suggests it is advantageous.

Tax planning and accounting methods

Sound tax planning and effective accounting methods can impact a company's tax liability. Properly structured financial transactions, deductions, and credits can reduce tax burdens.

Strategy: Work with tax professionals or consultants with expertise in Estonian tax laws. They can assist in structuring transactions to maximise tax efficiency. Make sure you keep accurate records and financial reporting to support tax deductions and credits.

Transfer pricing

Transfer pricing involves setting prices for goods, services, or intellectual property exchanged between related entities. Ensuring that these transactions are conducted at arm's length can mitigate tax risks.

Strategy: Establish and document transfer pricing policies that comply with Estonian regulations and international standards. Consistently review and adjust prices for intra-group transactions to align with market conditions and demonstrate compliance with transfer pricing rules.

Utilising tax credits and deductions

Estonia offers different tax credits and deductions to incentivize specific activities and investments. These can significantly reduce corporate tax liabilities.

Strategy: Identify available tax credits and deductions that apply to your business. Examples include research and development tax credits, investment incentives, and green tax benefits. Make sure that your business meets the criteria to take full advantage of these incentives.

Managing dividends and capital gains

Managing the timing and nature of dividends and capital gains can impact tax liability, especially for shareholders.

Strategy: Consider strategies such as:

- Timing dividend distributions to align with shareholder needs and tax planning opportunities.

- Managing capital gains by optimising the sale of assets and considering the tax implications of investments.

- Exploring tax treaties to minimise double taxation on dividends and capital gains when dealing with foreign shareholders or investments.

If you’re able to use some of these strategies when planning your corporate tax, you will be able to minimise the tax liability of your business. This will help pave the way for growth and financial stability.

Unlocking tax incentives in Estonia: Maximising benefits and compliance

As well as being a great place to run your business from generally, Estonia also offers a range of tax incentives. These are designed to stimulate economic growth, innovation, and investment. They are also used to attract businesses, both domestic and international, and provide them with opportunities for cost savings and growth. If you want to take full advantage of these incentives, while staying tax compliant, it’s important to understand the programs. Here are some key tax incentives in Estonia and strategies for maximising their benefits:

Research and Development (R&D) tax credits

Estonia encourages innovation and R&D activities through tax incentives. Businesses engaged in eligible R&D activities can benefit from tax credits to reduce their corporate tax liability.

To make the most of R&D tax credits you should:

- Document R&D activities comprehensively to support your claims

- Ensure that your R&D projects align with Estonian tax regulations and guidelines

- Collaborate with research institutions to leverage their expertise and potentially access additional incentives.

Investment support measures

Estonia offers investment support measures to attract foreign and domestic investment. These measures include different incentives to support business expansion and job creation.

When considering investment in Estonia you should:

- Research available investment incentives, including grants, subsidies, and tax benefits

- Collaborate with Estonian government agencies and local authorities to understand and access available support

- Ensure compliance with investment requirements and reporting obligations to maintain eligibility for incentives.

Startup incentives

Estonia has become known as a thriving hub for startups. The country offers a lot of incentives for startups to foster entrepreneurship and innovation.

To leverage startup incentives you can:

- Register your business as a startup if it meets the eligibility criteria

- Explore tax exemptions, reduced labour costs, and access to venture capital

- Engage with Estonia's startup ecosystem, including accelerators and innovation programs.

Green tax benefits

Estonia promotes environmentally responsible business practices by offering green tax benefits. These incentives aim to reduce the environmental impact of companies while providing tax advantages.

To benefit from green tax benefits you can:

- Implement eco-friendly practices and technologies in your business operations

- Research available green tax incentives, such as reduced energy taxes and exemptions

- Ensure compliance with environmental standards and reporting requirements.

Export and international trade opportunities

Estonia's strategic location, well-developed logistics infrastructure, and access to international markets make it an ideal base for export-oriented businesses. The country offers a number of incentives to support export activities.

When exploring export and international trade opportunities you can:

- Utilise Estonia's free trade agreements and trade partnerships to expand your global reach

- Investigate export-related tax incentives and customs duty reductions

- Engage with export promotion agencies and industry associations for guidance and support.

This overview of Estonia’s corporate tax landscape should help you when setting up your business, or if you’ve already started your business from Estonia. Keep an eye on the wamo blog for more features about doing business in Estonia.